UK Tax Calculator: Stop Overpaying & Find £2,000–£15,000 in Hidden Savings

TaxPilot analyses your salary, pension, childcare, and benefits to find the exact adjustments that save you the most money.

Free to start. No accountant needed.

See how it works in 2 minutes

The Tax Traps You Can't See

The £100k Trap

Earn £100,001–£125,140? You're paying an effective 60% marginal tax rate. Every £2 you earn over £100k costs you £1 of personal allowance.

A £5,000 salary sacrifice could save you £3,000+ in tax.

Lost Childcare Benefits

If either parent earns over £100,000 ANI, you lose 30 Free Hours (worth £6,000+/child/year) and Tax-Free Childcare (£2,000/child/year).

TaxPilot shows exactly how much pension sacrifice unlocks these benefits.

The Invisible Marginal Rate

Your take-home doesn't reflect your true marginal rate. With NI, student loans, HICBC clawback, and PA taper — you could be losing 60–70% of every extra pound.

TaxPilot calculates your real rate and shows how to reduce it.

How It Works — 3 Steps

Enter Your Details

2 minutes. Salary, bonus, pension, benefits, children. Six tabs, all optional — start with just your salary.

See Your Full Picture

Instant. Monthly breakdown, tax band analysis, childcare eligibility, pension allowance — all calculated live.

Tax: £19,432

NI: £5,892

Optimise

The aha moment. Toggle 'Optimised' to see how a single change affects every number. Ask the AI advisor.

Save £2,400/year

Powerful Features

Six tools working as one continuous cycle — powered by AI

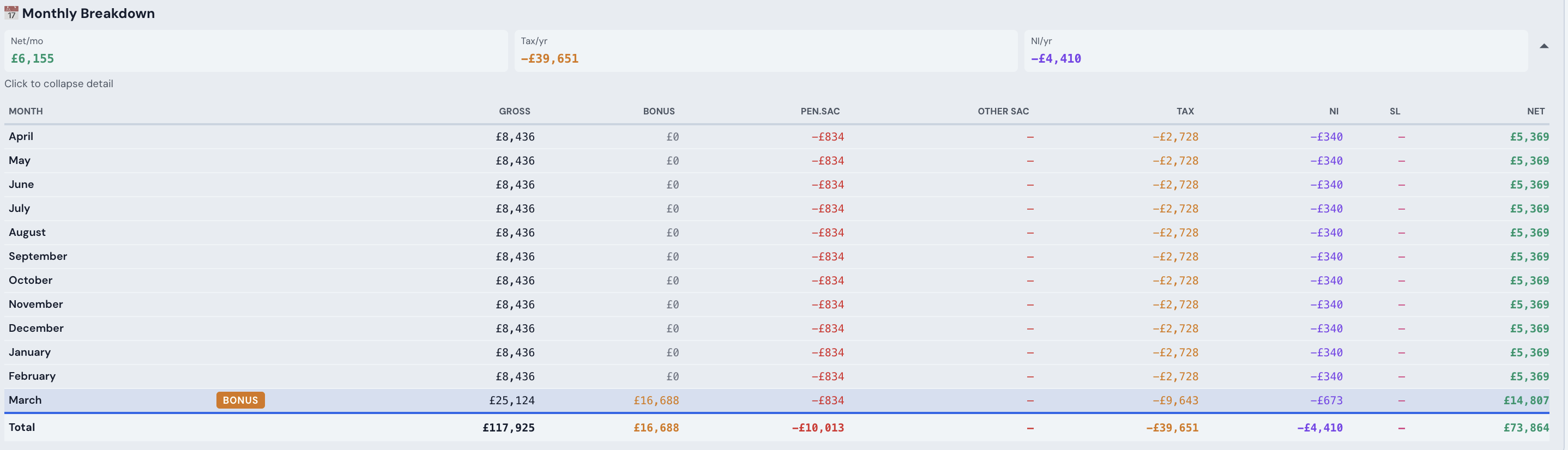

Monthly Breakdown

Toggle between current and optimised to see exactly when your take-home changes. Bonus months, car sacrifice start dates, nursery start dates — all pro-rated correctly.

See Your Savings Instantly

Trusted by UK Professionals

"I was paying £18,000/year for nursery. TaxPilot showed me that a 4% pension increase unlocks 30 Free Hours — now I pay £9,200 and have £4,800 more in my pension."

— Senior Developer, London

"I didn't realise my £105k salary put me in a 60% tax trap. TaxPilot saved me £3,200/year in 10 minutes."

— Product Manager, Edinburgh

"Finally a tool that actually explains why my take-home barely changed after my pay rise. The optimisation suggestions are quantified, not generic."

— Finance Manager, Manchester

Simple, Transparent Pricing

One-time annual payment.

Free

Forever free

No credit card required

Pro

Everything you need to optimise

per year (one-time payment)

A tax advisor charges £75–£150/hour

TaxPilot: £69/year — pays for itself in the first week

Frequently Asked Questions

Is this regulated financial advice?

No. TaxPilot is an informational tool that helps you understand your tax position. We recommend consulting a qualified tax advisor or IFA before making significant financial decisions.

Is my data safe?

All calculations happen in your browser. We don't store any financial data on our servers. Your inputs are saved to your browser's localStorage only. Authentication uses Supabase (email only), and payments are handled by Stripe.

What tax years are supported?

2024/25, 2025/26, 2026/27, 2027/28, and 2028/29 (projected). We update rates as HMRC confirms them.

What's the difference between free and Pro?

Free gives you a full tax calculator with monthly breakdown. Pro unlocks the optimisation engine — Sacrifice vs Pay analysis, the Optimised view toggle, pension AA tracking, household scenarios, and unlimited AI advisor access.

Your Tax Position Won't Optimise Itself

Start in 2 minutes. See your savings instantly.